audit working papers meaning

Audit working papers refer to the documents prepared by auditors when collecting evidence. Working papers represent the volume of work performed by the auditor and his staff.

What Is Audit Working Paper

Provide assurance that the work delegated by the audit partner has been properly completed.

. Hence they enable the easy drafting and preparation of a detailed audit report. Are necessary for audit quality control purposes. Audit working papers refer to the document in which the auditor writes facts data analysis of accounts while performing an audit of the enterprise.

Working papers are important because they. According to ISA 230 Audit Documentation the auditors objective is to. A any audit evidence obtained by the Service Provider from the Agency.

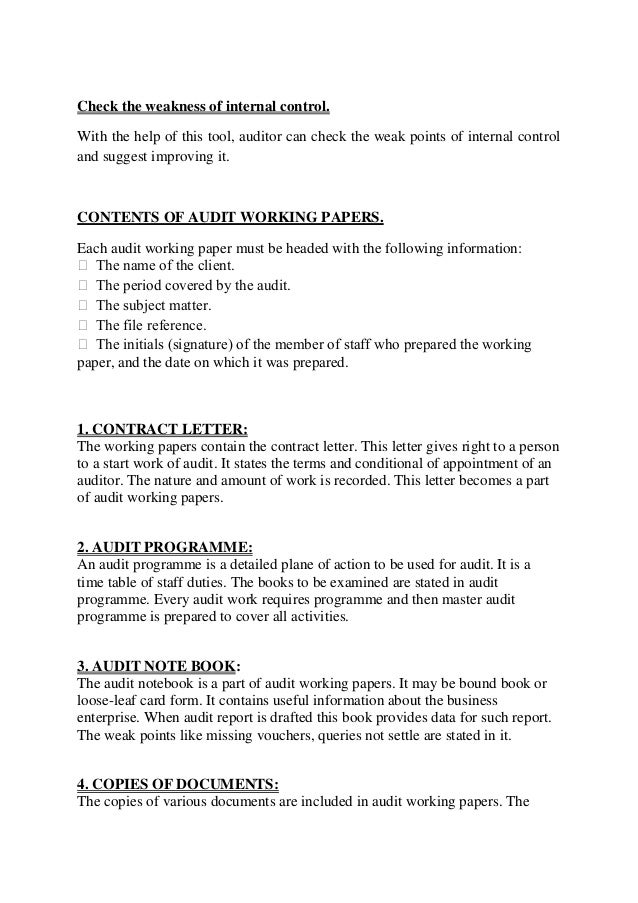

In other words working. Contents of audit working papers. It is a written record that an.

Audit working papers are the documents which record during the course of audit evidence obtained during financial statements auditing internal management auditing information. The audit working papers constitute the link between the auditors report and the clients. While the finished product of an audit engagement is a well-written and clear audit report working papers are the most important documents in an audit.

Audit working papers are documentation prepared and organized by the auditor to perform a proper audit service. Working papers hold a record of matters of. Audit working papers are the outcome of the documentation process.

Audit_working_papers_6docx - AUDIT WORKING PAPERS MEANING. Audit Working papers contain adequately detailed and up-to-date facts which defend the fairness of the auditors conclusions. B the Service Providers.

Audit working papers are the documents which record all audit evidence obtained during financial statements auditing internal management auditing information systems. Audit working papers are the documents. Audit working papers are the documents that record all audit evidence obtained during financial statements auditing internal management auditing information systems auditing and.

Working papers are the record of various audit procedures performed audit evidence obtained allocation of work between audit team members etc. It includes a record of various audit procedures that auditors perform the evidence they collect. Working papers are informational reports prepared by accountants and auditors as supporting documents for formal reports and financial statements.

Audit working papers means where a component of the Services includes audit services. The working papers constitute complete and conclusive evidence in future as to the entirety and completeness of the audit work. Working papers are the record of various audit procedures performed audit evidence obtained allocation of work.

AAS 3 states working.

Audit Working Papers Types Characteristics Information

Meaning Of Audit Working Papers In Hindi Accounting Seekho

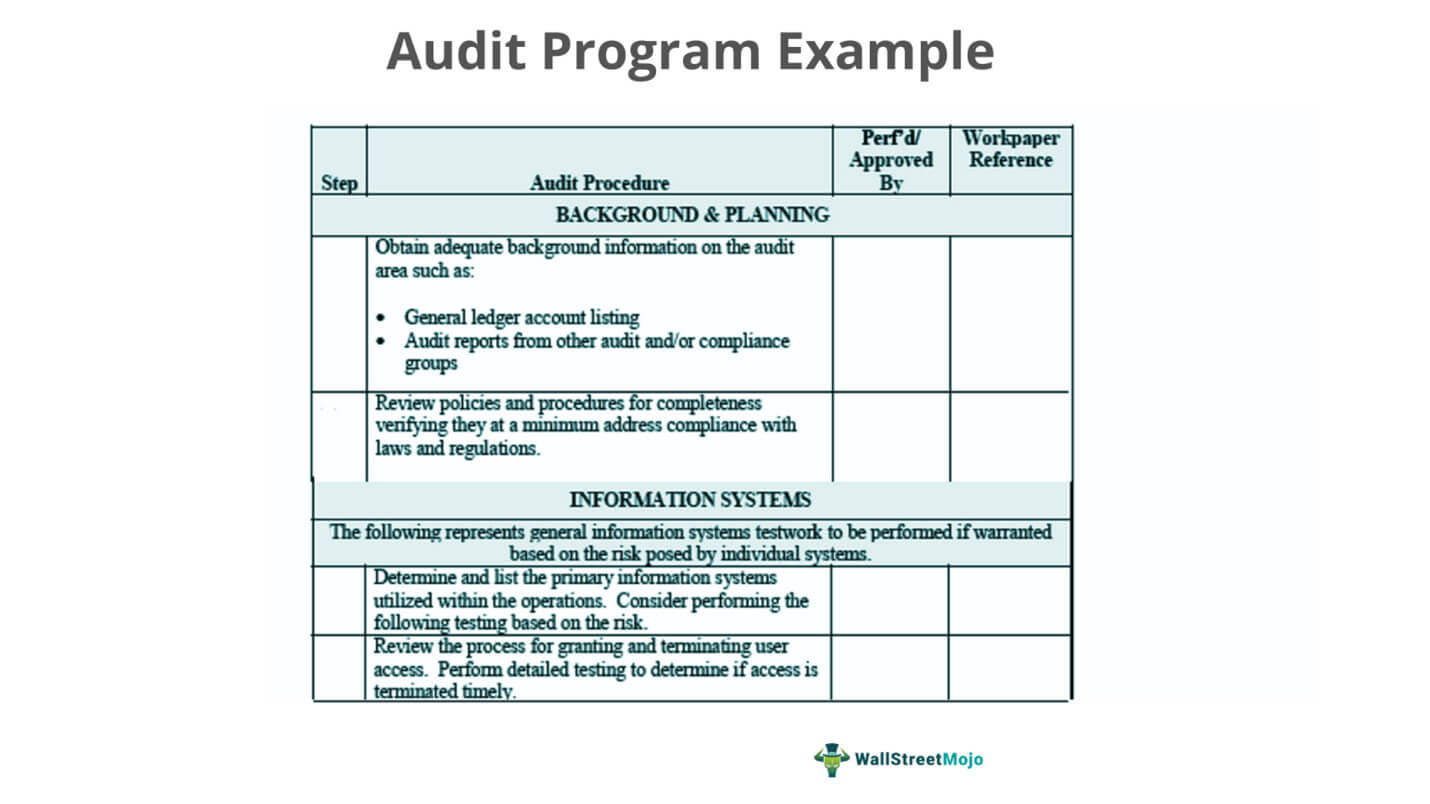

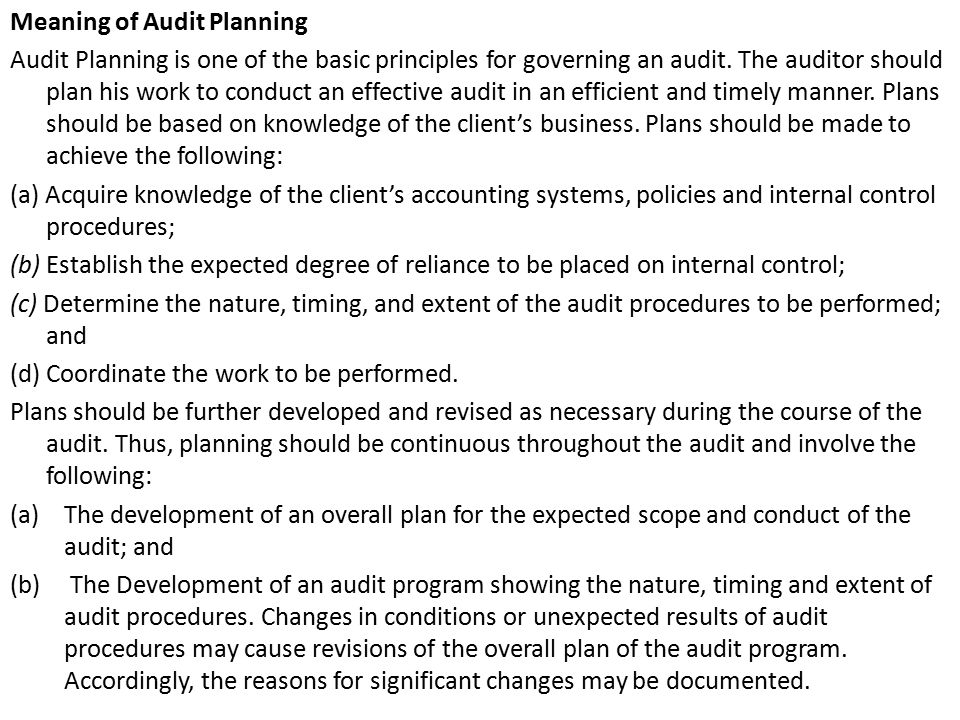

Audit Program Meaning Objectives Types Samples

Audit Working Papers

/audit-envelope-are-you-prepared-on-white-paper-an-yellow-envelope-holding-by-human-hands-1036260604-c9131ff9a9774a98a5c0edb05cf0690c.jpg)

Generally Accepted Auditing Standards Definition Gaas Vs Gaap

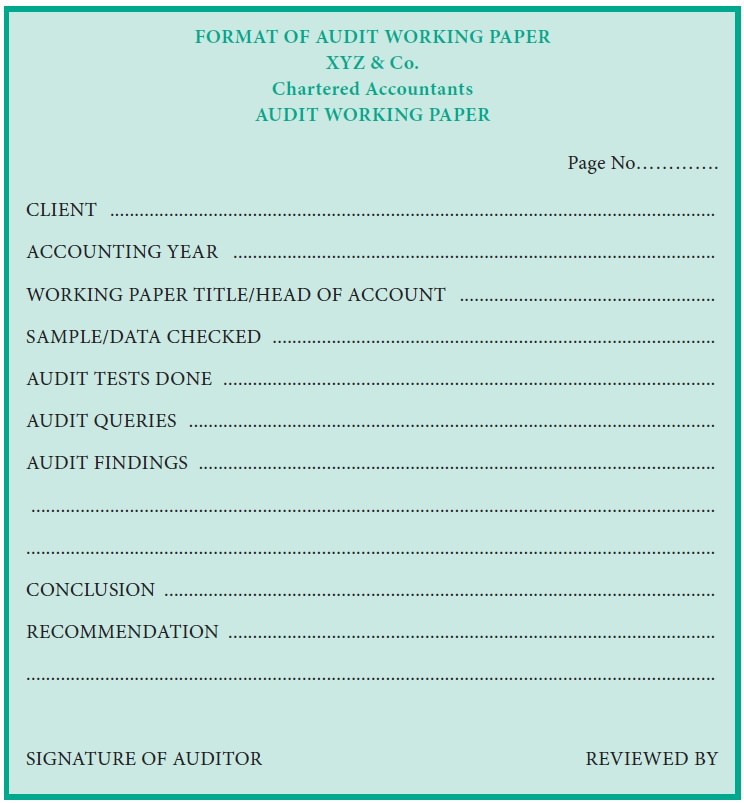

Audit Working Paper

Auditing Questions Meaning Objectives Audit Momorandum Audit Notebook Audit Working Papers Youtube

Audit Working Papers Meaning Definition Contents Objectives Importance Or Advantages Auditing

Meaning Of Audit Working Papers In Hindi Accounting Seekho

Audit Planning And Developing An Audit Program Audit Working Papers Lecture Ppt Download

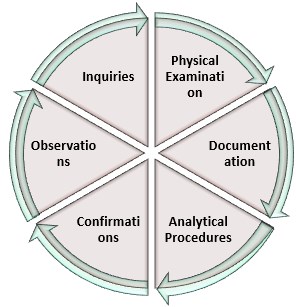

Audit Evidence Meaning Example Top 6 Types Of Audit Evidence

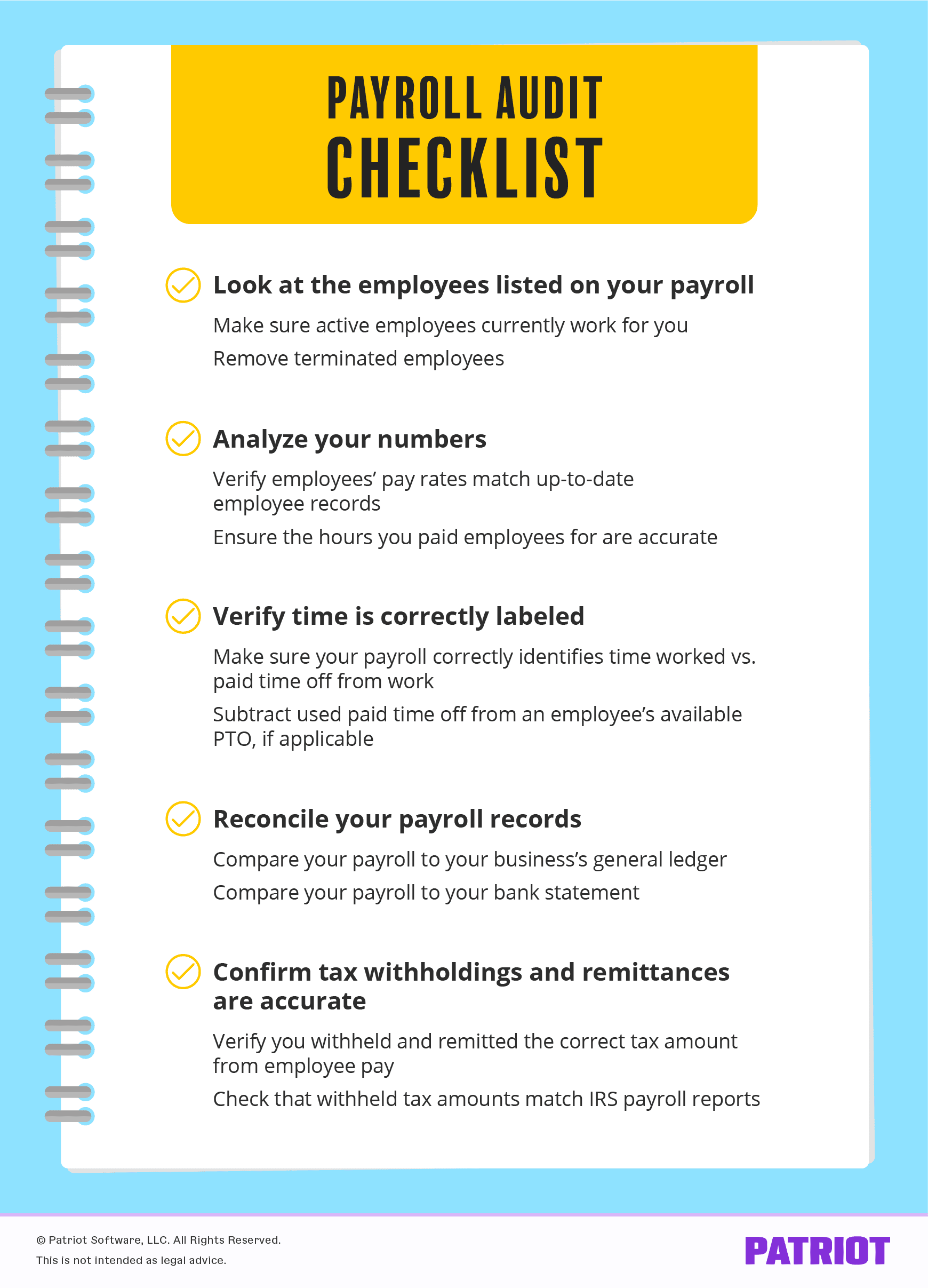

Payroll Audit Definition Benefits Procedure Checklist

Audit Working Paper Pdf Internal Control Audit

Audit Evidence Meaning Example Top 6 Types Of Audit Evidence

What Is Audit Working Papers Meaning Content Importance And Ownership And Essential Youtube

Audit Working Papers Importance Characteristics Contents And Example

Auditing Tutorial Practive Question Auditing Tutorial Audit Documentation Q1 Audit Studocu

Documentation Sa 230 R Pdf Internal Control Audit

Study Adda Important Of Auditing Working Papers How To Plan Paper Meant To Be